Access Advantage

Until now, alternative investments have primarily been the domain of large institutional investors such as pension funds, endowments, and insurance companies. Many advisors and investors have had limited or, in many cases, no ability to source and access top managers of private strategies.

Even when an investor can gain access, basic due diligence and high minimum investment thresholds can still be obstacles.

As a single entity, Independent Access Partners is able to offer our individual investors:

- Lower initial investment minimums

- Lower fees and favorable terms that are passed along to our investors

- Rigorous and repeated due diligence

Our mission is to deliver fiduciary-first private investment solutions to advisors and investors that will provide value to all parties involved. We want to see private placements more widely accessible to investors and advisors, enhanced Limited Partner terms, and enable General Partners to reach new sources of capital.

Important facts to know before investing in Private Real Estate, Private Equity, or Venture Capital, like those in ORE Fund I.

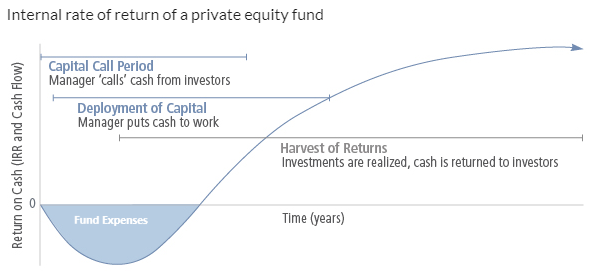

1. J-Curve:

This is perhaps the most important characteristic because many investors are accustomed to immediate positive returns from an investment. During the early years of a fund, Limited Partners (IAP Investors) pay fees to the General Partner in the form of management fees, structural costs (Administration, Audit, Accounting, etc.), and early investor catch-up*. The portfolio typically does not have enough positive returns to overcome the early fee burden. Investors should expect a negative return during the beginning of the investment period, but will likely dissipate over time and produce a “J” like return profile (See diagram, right).

IAP ORE Fund I has done a number of things to mitigate the J-Curve, however, it still will still experience an initial decline. Below are some of the examples of actions taken to minimize the dip of the J-Curve:

- No Management fee or Performance based fees being taken by IAP

- IAP has minimal structural costs (Audit, Administration, Accounting) – approximately 40 bps annually

- Reduction in CapRidge’s Management fee and performance fees

2. Performance Measurement:

Private Real Estate, Private Equity, and Venture measures its performance using am internal rate of return (IRR) calculation. While public securities are evaluated using a time-weighted return (TWR). It is difficult to measure TWR for Private investments due to drawdowns (capital calls) over time, large moves in valuations, and lumpy distributions. The IRR calculation tends to be more accurate and incorporates timing and gains relative to the amount invested.

IAP and our administrator (UMB), will be able to provide the appropriate information to reflect proper performance measurement to the Client Portal. Clients/investors will also have access to the UMB Alts portal to access their capital statements and tax information.

3. Infrequent Pricing:

While public securities price daily, private markets typically will not price not more frequently than quarterly. The general Partner will follow GAAP accounting principles to provide an estimated market value. These values are produced in conjunction with the funds annual third party auditor. An Audit of the fund is produced annually.

IAP will expects capital statements will be available to investors 50 days following the quarter end on the UMB alts portal. The information will reflect a partial 4th quarter of 2019 investment in the CapRidge Fund IV and the 3 separate co-investments.

*Early Investor Catch-Up: Also call a “True-Up”. The subsequent investors are required to compensate the initial investors for the fact that the initial investors have had their capital tied up in the fund for longer. This is an interest compensation charge and it is based on the capital amount from the subsequent investor, an agreed interest rate, time apportioned for the time between the initial and the subsequent closing. This equalisation interest is not due to the fund. It is incurred by the subsequent investors and paid to the initial investors.

Typical Private Equity J-Curve